Why Is PLTR Swinging So Much Lately? Let’s Look at Government, AI, and Valuation in One Shot

This post looks at PLTR by weaving together the defense/government AI story, the 2026 growth outlook, and the question of “why are people piling in even at this price,” focusing on what to be cautious about and what to watch over the next 3–12 months in a conversational way.

💡 3-Second Key Takeaways

- The reason PLTR moved today is that news on defense/government AI contracts and an aggressive 2026 growth outlook came out together, reviving its image as a “government+AI” flagship.

- On the flows side, money chasing defense/AI themes continues to come in, while short-term profit-taking and short covering overlap, so trading feels way heavier than usual.

- Right now it’s already pretty expensive, so I’m more in the camp of “I get the long-term growth story, but for the short-term price action, it feels better to watch slowly while checking earnings.”

🔍 Evidence & Claims

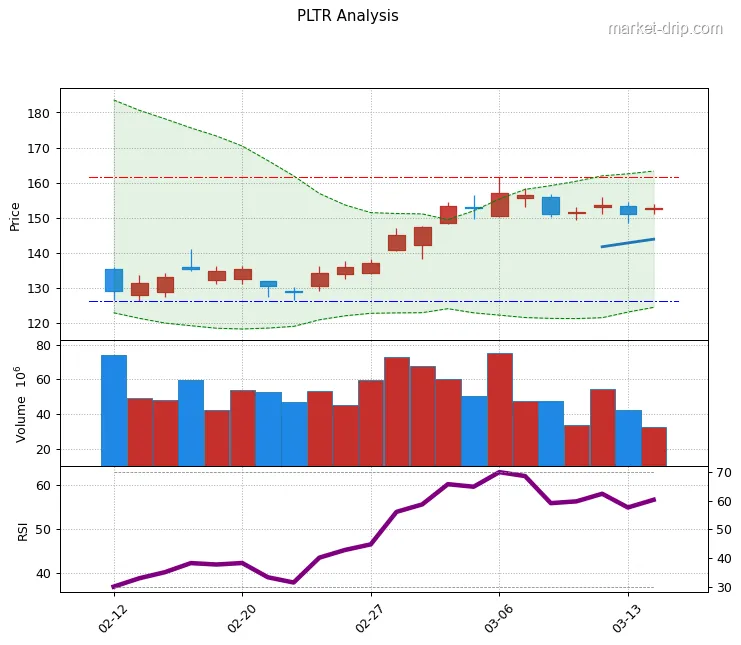

- Write the single most important observation from today’s price/volume. [Source]

Market Story

With geopolitical tensions rising, talk around defense spending has grown, and the idea that the U.S.

needs to lay AI more deeply into its data/intelligence systems is gaining strength.

Against that backdrop, PLTR has been rolling out back-to-back announcements on contracts with the Department of Defense and Department of Homeland Security, which has really amplified the view that “if it’s government-side AI software, isn’t it basically these guys?” On top of that, the company put out guidance that it will significantly grow revenue in 2026 versus the prior year, which stapled a “growth story” onto the narrative.

So today in the market, PLTR isn’t really being treated as just another tech stock; it’s more like a name where policy, security, and AI narratives are all tangled together at once.

🔍 Evidence & Claims

- The key point from a policy/regulatory or narrative perspective. [Source]

Price Trends & Momentum

Unlike previous phases where it would correct for a while and then stair-step higher again, this time it’s more like it spikes sharply whenever a defense/AI headline hits and then gets smacked back down, showing more jumpy action.

Compared with the big AI tech names, the price swings are wider and more violent up and down, so for a conservative index investor, it’s natural to think “this just has to be treated as a single-name theme trade.” That’s why this zone is hard to call either a clearly broken trend or a comfy dip to buy; it sits more like a middle area where short-term sentiment is wobbling back and forth.

Key Catalysts & Risk Factors

One is the expansion of defense/government AI contracts; the other is the company’s projection that revenue will grow sharply in 2026 versus the prior year.

As of 2025, U.S.

government revenue is still a large share of the total, and the fact that this piece grew strongly year-on-year has been emphasized, giving people some comfort that “policy and budgets are holding up.” At the same time, the company itself talking about significantly boosting revenue in 2026 has people wondering “maybe the AI pipeline is bigger than we thought.” But the risks are clear too.

If defense/government budgets slow faster than expected, or if the AI regulatory stance tightens more than anticipated, the growth premium it’s been enjoying can be the first thing to get cut, and that high P/E can quickly flip into a burden.

In a macro downturn where rates wobble again or the economy softens, the combo of “growth stock + government contracts” can actually increase volatility instead of cushioning it, which is another angle worth keeping in mind.

Recent News & Developments

government; second, a strong 2025 earnings print; and third, aggressive guidance for 2026. On the defense side, chunky contracts with the Department of Defense and Department of Homeland Security reinforced the perception that this company is “not just a general SaaS name but a defense AI specialist solution.” On the earnings front, U.S.

government revenue was up sharply year-on-year and total revenue grew at a high double-digit rate, aiming to show that this is not just a theme story but one where the numbers are following through.

But if you read beyond the headlines, you’ll see that a lot of this is already baked into the share price, which is why articles tend to talk about “defense AI beneficiary” on one side and “valuation has run too far ahead” worries on the other.

🔍 Evidence & Claims

- One-line summary of the single most impactful news item. [Source]

Institutional & Insider Activity

Because active funds betting on defense/AI and retail traders are both piling in, the stock tends to react sharply to headlines at the open and then often gets whipped around into the close by short-term profit-taking and short covering.

On the options side, short-dated call activity is pretty noticeable, suggesting there’s a decent chunk of money targeting short-term events.

On the insider front, there have been several rounds of selling by management after past earnings, and recent behavior still looks more like “trimming in a strong price zone” than “bailing out completely,” according to some analyses.

Putting all that together, it’s more realistic to think of PLTR right now not as a name owned only by long-term conviction money, but as sitting in a “mixed zone” crowded with traders chasing short-term events and themes as well.

🔍 Evidence & Claims

- One notable feature in volume/options/flow. [Source]

Against NVDA and MSFT, Where Does PLTR Sit?

Those guys own the big pillars like chips, cloud infrastructure, and productivity software, whereas PLTR leans into “AI software specialized for data and decision-making,” so even within the AI theme, its role is a bit different.

On valuation, PLTR trades at a much higher P/E than those big names, which means the market is pricing its growth story more aggressively.

But because a large part of that growth still comes from defense/government, the structure comes with both the advantage of “relatively stable long-term contracts” and the drawback of being very “sensitive to policy and budgets.” So within the sector, PLTR is better thought of as sitting in a special spot that’s “strongly swayed by policy and AI narratives,” rather than competing on size or stability with the mega-cap AI players — the roles are clearly different.

🔍 Evidence & Claims

- A standout metric or market-share data versus peers. [Source]

Rates, Policy, War Headlines: PLTR in the Big Picture

If rates stay high, growth stocks generally feel the pressure, but in a regime where defense/government spending is maintained or increased, there’s a narrative that names with large government revenue like PLTR can be relatively less shaky.

As geopolitical tensions rise, the chance of more spending on defense and intelligence infrastructure also rises, which can make the combination of defense and AI at PLTR look like an opportunity.

But if AI regulation tightens, data usage and model deployments can slow down, and government contracts may have to go through more layers of review, raising concerns that the current fast revenue growth picture could decelerate.

In short, on the big stage, PLTR is basically sitting where “defense/government spending expansion” and “AI regulation tightening” are playing tug-of-war over its future.

🔍 Evidence & Claims

- Key way macro or policy changes affect company earnings. [Source]

Investment Plan (3–12 Months)

📈 Bull Case

If we sketch the positive scenario, it looks like this: defense/government AI budgets keep growing as they are now, PLTR signs more long-term deals with these agencies, and the company actually delivers on its projection of sharply higher revenue in 2026 versus the prior year.

If, on top of that, the commercial segment gradually grows its share and eases the “over-reliance on government” concern, the market might be willing to give it an even higher premium than today.

In that case, even if there are short-term pullbacks, as long as the belief that “eventually the numbers back it up” holds, the medium- to long-term uptrend can continue — that’s basically the optimists’ argument.

📉 Bear Case

The negative scenario is the flip side: defense/government budgets slow faster than expected, or AI regulation tightens more than expected, bringing down the pace of new deals and revenue growth.

PLTR is already trading at a high P/E, so even a slight slowdown in growth could prompt the market to cut the premium first on the grounds that “it’s too expensive.” In that setting, if the macro backdrop also worsens, we can’t rule out the possibility of a prolonged, frustrating range where even good news doesn’t move the stock as strongly as it used to.

💡 Investment Strategy

So from a strategy perspective, instead of rushing to build a big position in PLTR right now, it may feel more comfortable to check, quarter by quarter, how much of its 2026 growth promise it is actually delivering and adjust your thinking as you go.

Since the defense/AI theme is so strong, sharp rallies and selloffs can repeat around short-term events, and rather than chasing those moves emotionally, having your own view of fair value and risk tolerance and easing in gradually can help reduce mistakes.

To put it in one line, it’s the kind of stock where “the story is flashy and the price already reflects a lot of it,” so instead of falling for the story first, it suits investors who can watch the numbers and policy together and pace themselves.

🔗 References & Sources

Frequently Asked Questions

Q. Honestly, it already ran a lot in 2025 — if I get in now, am I just buying the top?

That’s why this zone is less about “instant profits” and more about watching how much of the 2026 growth story the company actually delivers, then making slower decisions that match your own time horizon.

Q. With this much reliance on government contracts, if policy directions change one day, isn’t that game over?

But thanks to that same structure, there are also long-term contracts in place, so rather than everything disappearing overnight, it’s more like growth slows as budgets are cut or regulation tightens, and the stock price reacts ahead of that process.

Q. Compared with names like NVDA or MSFT, is there any real reason to bother with PLTR?

So if we really force a role split, the former are “solid AI infrastructure,” and PLTR is more of a “defense/government-attached AI story play,” which makes it easier to see that they serve different purposes within the AI space.