Oracle (ORCL) jumps 9% after earnings – is it finally a real AI winner?

In this post, we’ll walk through why Oracle (ORCL) ran more than 9% in the day following its Q3 earnings, using core numbers like EPS, revenue, and cloud growth along with the **AI infrastructure story** so you can get a feel for whether this is real strength or just short-term heat.

💡 3-second TL;DR for this trade

- Today ORCL spiked about 9% in after-hours plus the next session’s regular trading, off Q3 earnings that beat expectations and an AI cloud growth story that got bundled on top.

- On the flows side, trading volume jumped well above normal after earnings, with what looks like a mix of institutional and short-term trader money piling in all at once.

- Since the stock already moved a lot in one go, from here it feels like a zone where you think about both further upside and a near-term pullback, and where scaling in tends to feel more comfortable.

🔍 Evidence & Claims

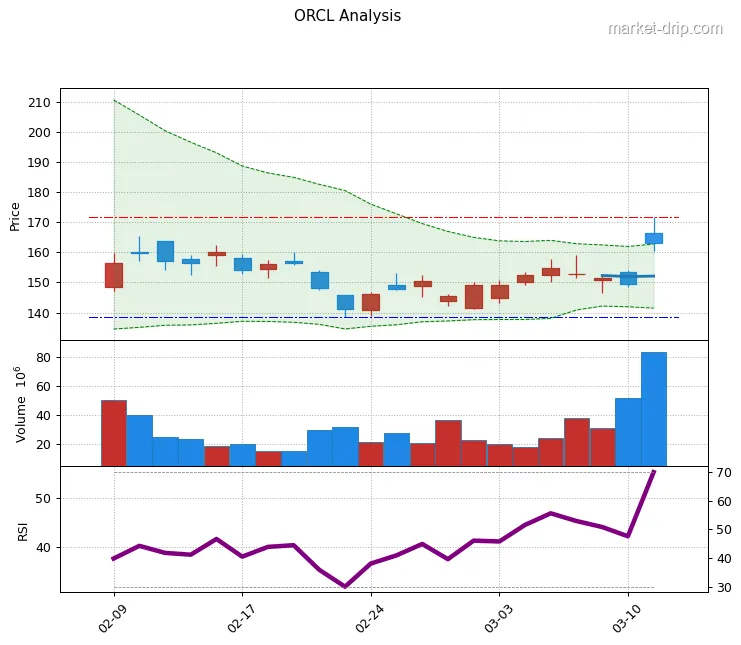

- Write the single most important observation point about today’s price/volume action. [Source]

Market Story

ORCL dropped its Q3 earnings right after the prior close, ripped in after-hours, and then kept that move going through pre-market and the regular session, ending up roughly 9% higher in total.[web:53][web:61] That’s not a “pretty good quarter,” that’s the market saying the numbers were genuinely surprising.

Once you look at the figures, the mood gets even clearer.

This quarter, Oracle posted adjusted EPS of 1.79 and revenue of about 17.19B, beating Wall Street’s 1.70 and 16.9B on both lines.[web:52][web:46] On top of that, they raised their 2027 revenue outlook to 90B, basically saying, “The AI infrastructure capex boom is very real for us too.”[web:50][web:60]

There wasn’t some special policy or regulatory catalyst here – this is a pure private AI investment story driving things.

With money pouring into AI data centers and cloud infrastructure, Oracle came out and proved with numbers that “we actually have a real seat at this table,” which is exactly the kind of setup that gives you a sharp, one-day re-rating like today.[web:63]

🔍 Evidence & Claims

- From a policy/regulation or narrative angle, what is the single key point? [Source]

Price Trends & Momentum

It was still well off last year’s highs and had spent the recent months getting hit whenever the broader market wobbled – classic “waiting on a catalyst” price action.[web:55] Then you get a 9%-ish one-day spike on earnings, and visually it really does look like “okay, we’re finally trying to break the range to the upside.”

If you widen it out to the sector, AI leaders like Nvidia and the other usual suspects have already been running, which makes ORCL look more like a late-joining AI infra runner.[web:63] When names like that finally catch a good earnings catalyst, it’s quite common for them to move a lot more than the index or the average cloud stock.

This 9%-range jump fits that pattern pretty nicely.[web:61]

But on a day with a move this big, it’s better to treat today’s candle as a “turning point signal” rather than proof that it’ll go straight up from here.

The real question is what the next few days and weeks look like: do you get a staircase move, or a pullback and then another leg – that part is still very much undecided.[web:62]

🔍 Evidence & Claims

- The single most important observation versus chart/momentum/sector. [Source]

Key Catalysts & Risk Factors

Oracle printed adjusted EPS of 1.79 and revenue of 17.19B, beating expectations on both, and overall revenue growth came in well above 20%.[web:55][web:46] The standout, though, is cloud: total cloud revenue was around 8.9B, up 44% year over year, and within that, cloud infrastructure revenue alone grew a crazy 84%.[web:53]

The second engine is the forward story.

Management lifted its 2027 revenue target to 90B, effectively laying out a path that assumes AI infra demand stays strong and keeps pulling their numbers up.[web:50][web:60] For the market, the scariest question is “when does the AI boom cool off,” and Oracle more or less just said, “we think we’re good at least through 2027,” which is exactly the kind of thing that makes a stock squirm higher.[web:65]

But the risks are just as clear.

First, growth at this pace is heavily tied to AI infra capex and a handful of big customers, so if that investment cycle slows or a major contract stumbles, the numbers can roll over fast.[web:53][web:63] Second, when you rip more than 9% in such a short window, valuation gets dragged up with it, which means that without a steady stream of good news, the stock is at risk of going sideways or giving some back.

Today’s rally is a combo of “higher AI infra expectations” and “confirmed growth,” but that also means the bar has just been raised quite a bit.[web:64]

Recent News & Developments

First line is something like: “Oracle beats Q3 with EPS 1.79 and revenue 17.19B, raises 2027 revenue target to 90B as AI data centers drive 44% cloud growth.”[web:52][web:50] Next line: “Cloud infrastructure revenue jumps 84%, with AI training and inference demand outpacing the company’s current capacity.”[web:53]

The last line is about sentiment.

CNBC, Reuters, and various research shops are basically saying, “The results were stronger than expected and helped ease worries about Oracle’s AI infra strategy,” framing this print as a kind of “relief event” in the middle of AI bubble concerns.[web:59][web:65] That’s why today’s rally is more than just “a nice quarter” – it’s the market warming up to the idea that Oracle isn’t just surviving the AI era, but may actually be becoming a meaningful pillar within it.[web:63]

🔍 Evidence & Claims

- One-line summary of the single most important market-moving news. [Source]

Institutional & Insider Activity

Right after the earnings drop, trading in ORCL call options jumped well above normal, and cash volume on the day and the next session pushed clearly above recent averages.[web:53][web:61] That pattern usually means a mix of institutions, quant funds, and short-term traders were all in the mix.

Even before earnings, there was plenty of chatter that “this one could move big this time,” and options pricing going into the event was implying a double-digit percentage move in the stock.[web:44][web:37] The company then delivered a print that cleared that bar, and on top of that you likely had short covering from traders who had been leaning bearish, which all together produced a 9%-plus rally like today.[web:62]

The open question is whether this ends up being a “one-and-done news spike,” or the start of more durable, medium-term money building positions.

If we keep seeing elevated volume for a while after this, it gets easier to argue that we’re shifting from a pure event trade into a broader repositioning phase.[web:61]

🔍 Evidence & Claims

- One notable trait from volume/options/flow. [Source]

Same table as MSFT and NVDA? Yes – but the feel is different

That’s why when you get an earnings print where both numbers and story line up, the stock can show more torque than the big leaders.[web:64]

The business mix makes the differences even clearer.

MSFT and AMZN are built around cloud as a core, and NVDA is literally the GPU/semiconductor engine, whereas ORCL still has a sizeable chunk of revenue coming from traditional database and enterprise software.[web:55] The twist this time is that Oracle just posted 44% cloud growth and 84% infra growth, which sends a strong signal that “their AI transition speed is faster than people thought.”[web:53]

So the clean way to frame ORCL is: it’s not yet a pure AI play, but more of a solid DB/software cash-cow base with an AI infra growth option layered on top.

That naturally means it has both a downside cushion from legacy businesses and an upside cap relative to the pure AI names – a trade-off that some portfolios might actually like.[web:60][web:66]

Rates and the AI cycle – how does that sound to ORCL?

When rates are high, the value of future cash flows gets discounted more heavily, which is a drag on growth stocks.

The fact that the stock still managed a 9%-plus pop here says, “Even in this rate environment, the growth and margins were strong enough to impress.”[web:26][web:61]

The other piece is the AI investment cycle.

The big market question right now is, “How long does this AI data center build-out really last?” Oracle, through its cloud/infra growth rates and the 2027 revenue outlook, is basically signaling that it expects robust demand for at least a few more years.[web:50][web:60] If global growth slows or policy shifts lead to IT/AI capex cuts, keeping these current growth rates will get harder, and at that point ORCL is likely to react more sharply to macro headlines.[web:65]

Bottom line, the macro backdrop isn’t perfectly friendly, but the AI infra investment theme still feels more like a tailwind than a headwind for now, and ORCL is one of the players catching that breeze reasonably well.[web:63]

🔍 Evidence & Claims

- Key way macro or policy shifts impact this company’s earnings. [Source]

Investment Plan (3–12 Months)

📈 Bull Case

Starting with the bullish scenario: the idea here is that what we just saw is “the beginning” rather than “the climax.” If AI infra and cloud demand stay as strong as they are now and the company keeps marching toward that 2027 90B revenue target, the market can keep re-rating ORCL from an old-school software name into a key AI infra pillar.[web:50][web:60] The stock already jumped more than 9% right after earnings and grabbed attention, but this could still be early innings of a bigger re-rating process in that story.[web:61]

📉 Bear Case

On the bearish side, you have to consider that this could be the point where “a lot of good news is already priced in.” If the AI investment cycle slows earlier than expected or macro conditions force companies to trim IT budgets, today’s 44% cloud growth and the 90B revenue outlook for 2027 might get revised down.[web:53][web:65] In that case, today’s 9% rally could easily retrace, leaving you with that frustrating situation where the business looks good on paper but the share price goes nowhere or even leaks lower.[web:62]

💡 Investment Strategy

In terms of strategy, this really comes down to temperament.

If you’re looking at ORCL after a 9%-plus pop like this, jumping in all at once carries obvious risk; for most people it will feel more comfortable to watch for pullbacks or short consolidation phases over the next few weeks and scale in.[web:61] If you buy into the AI infra·cloud theme and see ORCL as one of the players there, the practical approach is to keep an eye on whether the earnings numbers and that 2027 outlook hold up, and gradually build a position while watching both news and chart action.

In one line: it feels more like a “don’t rush, check its stamina while you get in” kind of timing than a “sprint now or never” moment.[web:53]

🔗 References & Sources

- Oracle Q3 FY26 Earnings Release

- Yahoo Finance - Oracle stock rockets higher on Q3 earnings beat, 2027 revenue outlook

- Investing.com - Oracle leaps on earnings beat, raised revenue guidance

- Yahoo Finance - Oracle Stock Surges 9% Post-Earnings: Cloud Revenue Jumps 44%

- CNBC - Oracle Q3 earnings report 2026

Frequently Asked Questions

Q. Am I the only one who missed this? It popped more than 9% in a day but local news barely talked about it.

Over in the U.S., people were already buzzing about EPS 1.79, revenue 17.19B, 44% cloud growth, and the 90B 2027 outlook.[web:52][web:53][web:50]

Q. If I buy now, isn’t it way too late? It’s already up 9%…

But since the company has now publicly put 90B in 2027 revenue on the table, watching whether they stay on track and scaling in over time can make it feel a lot less rushed.[web:50][web:61]

Q. Why even bother with ORCL when I can just stick to Nvidia or Microsoft?

Numbers like 44% cloud and 84% infra growth say, “this side is moving faster than expected too,” so some people see it as a different role to play inside a portfolio.[web:53][web:60]