MongoDB is running again? Why AI database expectations are heating up again

MongoDB isn’t just a database that developers like anymore, it’s treated as a name you can’t easily leave out of the AI·cloud infrastructure conversation. In this post, we’re going to organize what this current price zone means, using the simple question “why is it up again?” and tying together recent news, flows, and risks.

💡 3-second key investment takeaway

- Today MongoDB is seeing investor attention come back again on the back of AI·cloud database expectations and an upcoming earnings event.

- In terms of flows, money is moving back into growth stocks broadly, and because it’s seen as one of the key AI infrastructure names, it feels like it’s riding both the “theme + earnings” waves at once.

- Right now there is short-term momentum but also big valuation pressure, so it feels a bit more comfortable to see this as a phase where you worry more about “speed control” than just direction.

Market Story

In the UK Yahoo Finance trending ticker article, MongoDB is highlighted separately, which shows it’s being tagged as a “stock to watch now” among global investors.

On top of that, in the US, as earnings approach, interest is piling up around the question “will AI expectations show up in the numbers again this time,” and naturally both trading value and chatter are picking up here.

Rather than policy or regulation, this is a pure “theme + earnings” phase.

Last year it already got a big spotlight once as an AI·cloud database growth story, and since then, analyses pointing out that Atlas and other cloud services are still posting high growth rates have continued, so the market vibe is basically “this name is going to keep coming up in AI infrastructure talk,” and that perception is now fairly entrenched.

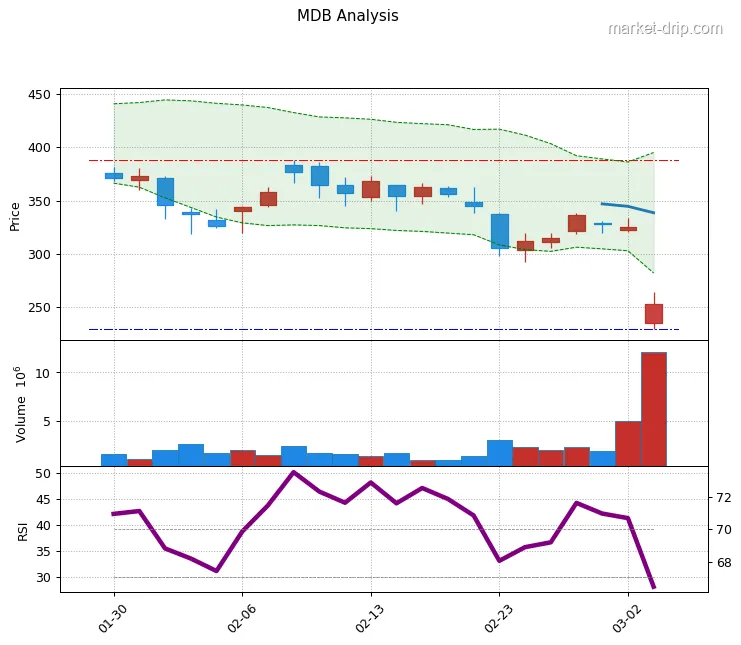

Price Trends & Momentum

After a big rally late last year on AI·cloud expectations, this year it’s been shaken by earnings jitters and rate worries, and more recently you can see attention rotating back in.

Compared with the indexes, even when Nasdaq growth stocks are in a breather, MongoDB tends to move more sharply on a single news item, so its swings are big.

Within the sector, names with the “AI infrastructure·database” tag tend to move hotter than general software names, so it’s good to keep in mind that this one is naturally a name with strong ups and downs.

Key Catalysts & Risk Factors

First, that cloud-based database services like Atlas are still maintaining high growth rates, and second, that the company is proactively reshaping its platform to fit AI applications.

The Voyage AI acquisition, and keywords like vector search and AI search feature enhancements support this story.

But the risks are just as big.

Above all, a lot of that growth expectation is already largely baked into the price, so even a small wobble in macro or interest rates can make the stock overreact.

On the competitive side, giants like AWS, Google, and Microsoft are all expanding their own databases and AI features, so the core battleground is whether MongoDB can keep showing developers clearly differentiated productivity and better experience.

Recent News & Developments

First, the warning pieces that say “if earnings and guidance don’t live up to the lofty AI expectations, the stock can swing hard down,” second, the more positive analyses that say “still, if you look at Atlas growth and AI infrastructure demand, the mid- to long-term story is intact,” and third, the preview-type pieces asking “will AI-related bookings and usage show up again in the upcoming earnings.”

For example, some outlets have pointed out that late last year MongoDB jumped sharply thanks to AI·cloud expectations, and since then Atlas revenue has grown to account for a substantial share of total sales.

On the flip side, more recent pieces warn that “when expectations are this high, even slightly conservative outlooks or hints of slowing growth can trigger double-digit drops,” so just from the news you can feel that “both sides of the scenario are wide open” for this stock.

Institutional & Insider Activity

Institutional ownership is relatively high, and many funds that bet on AI·cloud keep it as a position in their portfolios, so the broad stance leans more toward “we believe the long-term growth story.” At the same time, around earnings seasons, there have been repeated episodes of big swings over a day or two as targets and opinions were adjusted.

Especially if you look at articles from late last year and early this year, some analysts raised price targets and laid out more aggressive growth scenarios, while others used phrases like “if numbers don’t match the hype, disappointment selling hits fast,” showing a pretty big difference in tone.

So if you had to boil down the institution and big-player behavior at this stage to one line, it’d be something like: “basically holding for the growth story, but constantly adjusting the pace around earnings and news.”

Compared to rivals, what stands out?

This is a slightly different flavor from players like Snowflake, which is centered on data warehousing, or AWS and Azure, which bundle databases inside an entire cloud ecosystem.

From a developer’s perspective, once you learn it, it’s easy to use across many apps, and its structural flexibility is often cited as a strength.

On the other hand, compared with rivals embedded in huge platforms, MongoDB has the homework of having to prove everything itself from infrastructure to security and operations.

That’s why it’s proactively pursuing things like government and public cloud certifications, and building deeper partnerships with major cloud providers.

For investors, it’s easier to think of this as a battle over “how far it can establish itself as an independent option, not just one feature inside a big platform.”

🔍 Evidence & Claims

- MDB is targeting the AI·cloud market as an independent database platform, unlike Snowflake or AWS [Source]

Rates, economy, AI bubble: these three are the wildcards

First, how high rates stay and for how long.

Second, whether companies cut or increase their cloud·AI budgets.

Third, whether AI expectations pop as a short-term bubble or stay elevated longer than people think.

So far, whenever rates stabilize a bit, AI·cloud-related stocks have tended to rip higher in bursts, and MongoDB has moved alongside them as a kind of “AI database flagship.” If rates rise again or companies go back into cost-cutting mode, these types of growth stocks are usually the first to get hit, but if AI infrastructure investment lasts longer than expected, then today’s volatility might later just look like “mid-course bumps on a long growth story.”

Investment Plan (3–12 Months)

📈 Bull Case

In the positive scenario, we assume AI·cloud investment at least stays at current levels or increases, and that demand to modernize legacy databases keeps growing.

In that case, Atlas growth rates stay above a certain level, the Voyage AI acquisition and AI feature enhancements actually translate into new customers, and the market has room to re-rate this as a “growth story that lasts longer than feared.”

📉 Bear Case

In the negative scenario, you could imagine a situation where cloud·AI budgets are cut again due to another rise in rates or an economic slowdown.

In that case, even a slight deceleration in growth could trigger outsized reactions around earnings, because a lot of expectations are already priced in.

At the same time, if big tech doubles down on their own services, worries may gradually show up in the market that the slice MongoDB can capture is smaller than hoped.

💡 Investment Strategy

So if you think about a realistic strategy, it might feel a bit more comfortable to spread the risk across several names in AI·cloud infrastructure rather than trying to “win it all with this one stock.” Given MongoDB’s volatility, a pacing strategy—like trimming around earnings and then reassessing—is also worth considering.

If we boil it down to one line: “It’s a growth stock with a solid story, but because it can swing hard on news and rates, staggering your timing and sizing can make it less stressful to hold.”

🔗 References & Sources

Frequently Asked Questions

Q. Honestly, it already ran a lot last year then got hit… if I get in now, am I just buying the top again?

When AI hype was at its peak last year, MongoDB climbed a lot, and then it swung hard when numbers didn’t fully live up to those expectations.

So at this point, rather than “instant profit,” many people who believe AI·cloud investment could last a few more years are slowly scaling in with splits.

Q. Every headline just says “growth thanks to AI,” but is that actually proven in the numbers, or is it just fancy wording?

Cloud services like Atlas are taking up a bigger and bigger share of the company’s revenue, and there are analyses saying growth rates have been supported by AI app and data infrastructure demand.

That said, because market expectations are so high, there’s a track record of immediate disappointment selling when growth slows even slightly, so it’s also true that we’ve often been in that awkward zone where “the numbers are okay, but relative to expectations they feel iffy.”

Q. Every time Nasdaq drops, this name wobbles with it… if I can’t handle this kind of volatility, should I just avoid it completely?

When Nasdaq growth stocks wobble, MongoDB has often moved with them—or even more.

So if you hold it as a huge share of your portfolio, the day-to-day swings can be pretty stressful.

If that style feels heavy, mixing it with other names in the AI·cloud theme that move a bit less violently can be a much more breathable choice.