LGVN, the biotech stock that jumped 70% today — real opportunity or a one-shot trap?

Today’s LGVN move was not about earnings but about a capital raise of up to $30 million lining up with its clinical timeline, so the right lens is this: the company now has more breathing room financially, but dilution risk and volatility came with it.

💡 3-second investment takeaway

- LGVN is a U.S.

small-cap biotech that shot up more than 70% in a day after a private placement announcement for up to $30 million brought a dead-looking stock back to life. - The explosion in both volume and attention suggests the market is reading this not as just another news item, but as relief that the delisting scare has at least paused, mixed with short-covering.

- As of today, this looks like a zone where expectations and risk are both overheated, so a slow approach with time diversification and size diversification may feel more manageable than a short-term swing.

Market Story

LGVN had basically been forgotten as a nano-cap biotech, then it suddenly got pulled back into the center of the market after announcing a private financing deal worth up to $30 million.

The filing shows the company gets about $15 million right away in the first tranche, and the remaining $15 million can come later if trial results and stock-price conditions are met.

Why does that matter so much?

Because the company explicitly said this funding should support operations through 2026 Q4 and carry it to the readout of its key clinical trial, ELPIS II Phase 2b, expected in 2026 Q3.

From the policy and regulatory angle, this trial is tied to a rare pediatric heart disease, HLHS, so it is not an area where the FDA is simply closed off.

The company also framed this financing as directly tied to the next big pivot point, which is the 2b trial result.

So the market didn’t read today as just “they raised some cash.” It read more like “they now have a real shot to make one more serious push on the clinical story.” That is why the market narrative shifted in one day from “delisting fear stock” to “high-risk speculation candidate.”

Price Trends & Momentum

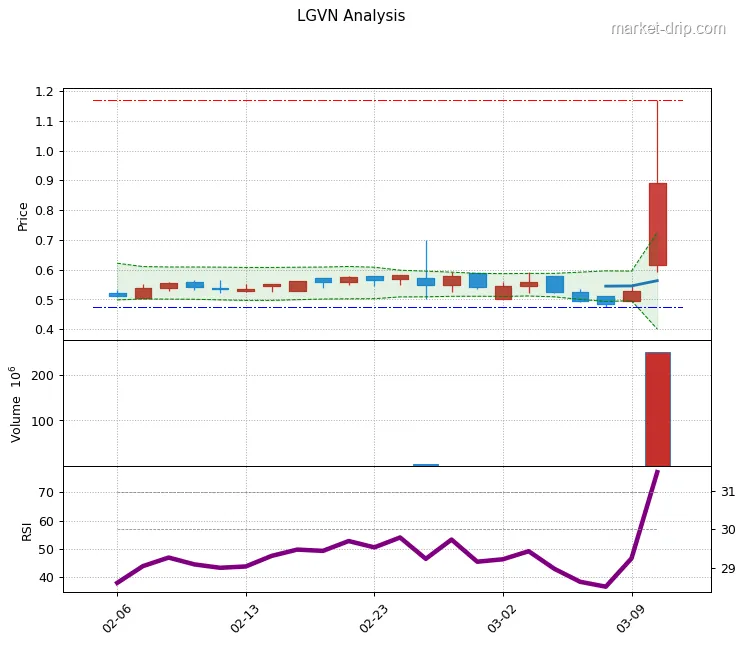

Until the day before, the market cap was hovering around the low tens of millions, then the stock jumped more than 70% on the funding news for up to $30 million, and suddenly the company looked very different in size.

Commentary also said volume surged by multiple times normal levels, and with the thin order book that is typical for micro-cap biotech names, the result was the kind of chart that swings wildly in both directions.

It looks even more extreme when you compare it with the sector and broader indexes.

On the same day, biotech and healthcare indexes were relatively quiet, while LGVN alone showed up near the top of Nasdaq gainers.

On days like this, the company’s core value usually has not changed in one session as much as market emotion has.

What really changed was the market’s short-term excitement around the financing and clinical setup.

So instead of asking, “Is this a normal pullback or crazy hype?” it may be more practical to ask whether this level of volatility is even within your own risk range.

Key Catalysts & Risk Factors

The key catalyst for LGVN is still the ELPIS II Phase 2b trial result expected in 2026 Q3. The $15 million it received now, plus the additional $15 million tied to conditions, is being presented as “breathing room capital” to keep the company alive through that clinical milestone and fund operations through 2026 Q4. If the trial goes well, the upside story gets much bigger.

The market could begin talking about options like orphan-drug benefits or a priority review voucher (PRV), which would make the upside imagination much larger.

On the other hand, the risk is even more straightforward.

The company still has almost no revenue, and past filings suggest annual revenue has remained only in the hundreds of thousands of dollars in recent years.

So this is not really a company surviving on business performance.

It is much closer to a company that depends almost entirely on clinical results and outside financing.

If the trial misses expectations, or even if the science looks decent but funding appetite dries up, the current $15 million may end up buying only a little time.

Keeping that possibility in mind helps today’s surge sound less magical.

Recent News & Developments

In the first tranche, the company issues about 6.01 million common shares at $0.52 per share, and it also issues convertible preferred stock that can later turn into common shares.

The company said this money is meant to fund operations through 2026 Q4 and cover the timeline through the ELPIS II Phase 2b data release.

It also stood out that names like Coastlands Capital, Janus Henderson Investors, Logos Capital, and Kalehua Capital joined the financing.

From the market’s point of view, that lineup is enough to create the feeling that “Okay, serious investors are at least willing to back this company through one more clinical shot.” But dilution is also very real here, so even after a good-news pop like today, the market can still circle back later and talk about future supply pressure.

Institutional & Insider Activity

As disclosed, institutions and funds such as Coastlands Capital, Janus Henderson, Logos Capital, and Kalehua Capital joined the private deal, which means at least $15 million is coming in on paper.

But we still do not know whether all of that money is truly “long-term hold capital” or whether some of it will rotate out around the clinical event.

Just looking at price action, the more-than-70% jump today and the volume spike feel like a mix of short covering and fresh short-term money chasing the move.

Some overseas articles also framed it as speculative demand rushing into a micro-cap biotech that suddenly got a financial lifeline.

But there is not enough public detail yet on short interest or options flow to say exactly how much of the move came from true long buyers.

So instead of saying, “Whales are in,” it is safer to say, “At least both the company and new backers have signaled they want one more serious shot at this level.”

Where LGVN stands among similar biotech names

Around mid-2025, its market cap was sitting in the low tens of millions, and even recent references still place it in a range around the low tens of millions rather than anything remotely large.

When you compare that with other rare-disease or cell-therapy developers at similar stages, plenty of them trade at market values in the hundreds of millions.

So the size gap here is very real.

But that tiny size is also why a story like today’s can produce such a violent reaction.

Other biotech companies at similar trial stages might raise money and move only a few percent, but LGVN was already tangled up in dilution concerns and delisting fears, so one financing deal flipped the whole narrative.

In valuation terms, this still trades much more like a pure event play driven by clinical results than like a normal operating business valued on revenue or cash flow.

That is probably the single biggest difference versus peers.

🔍 Evidence & Claims

- A standout metric or market-share data point versus peers. [Source]

How should you read this in the context of rates and the broader market?

In fact, the broader U.S.

nano-cap biotech space had a rough run during 2024-2025, and LGVN’s own market value also fell sharply over that stretch according to multiple data points.

Against that backdrop, seeing a number as large as up to $30 million in new funding matters.

At the very least, it suggests that some institutions still believe this company is worth backing through at least one more major trial event.

That said, the macro backdrop has not suddenly become friendly.

If rates move higher again, or if risk appetite fades across markets, high-risk biotech names like this are still likely to get hit first.

And because LGVN depends more on financing and clinical milestones than on operating results, its valuation can compress faster than usual when markets turn cautious.

So the right read here may simply be, “Biotech sentiment has opened a little breathing room,” while still asking how much pain the stock can take if the broader backdrop weakens again.

Investment Plan (3–12 Months)

📈 Bull Case

If you picture the positive scenario, it goes like this.

The financing of up to $30 million proceeds as planned in the $15 million + $15 million structure, and the ELPIS II Phase 2b result in 2026 Q3 lands in line with or better than what the market hopes for.

In that case, the story could quickly widen into things like a priority review voucher, a partnership announcement, or a stronger hand in negotiating the next funding round or a licensing deal.

If that happens, today’s more-than-70% jump may later look like it was not the end of the move at all, but just an early stage of the rerating.

📉 Bear Case

The negative scenario is actually pretty simple.

The first $15 million comes in, but the clinical result is mixed, or the market decides it is not good enough, and the second $15 million tranche never gets unlocked.

Then the current cash only buys time until funding pressure returns, possibly before 2026 Q4, and the market starts talking again about discounted stock issuance and more dilution.

If that happens at the same time as higher rates or a broader risk-off turn, even the institutions that came in this time could reduce exposure, and the stock could slide back toward its earlier nano-cap zone.

That is the classic “huge pop, then back to reality” pattern.

💡 Investment Strategy

Let’s talk practical strategy.

Honestly, with a stock like this, the story and the numbers are still both early, so it is hard to justify going all-in after a move like today.

For most people, it probably feels more manageable to allow only a very small position within the broader portfolio, and even then, to spread exposure over time rather than doing it all at once.

After a jump of more than 70% in one day, the key is to keep reminding yourself that this price already reflects a lot of emotion.

If I had to sum it up in one line: think of this as “a company that just earned one more shot at a clinical bet with up to $30 million in backing,” and view it with both hope and anxiety at the same time.

🔗 References & Sources

Frequently Asked Questions

Q. Honestly, it already ran 70% today — isn’t it too late now?

After a move of more than 70%, this clearly is not a clean short-term chase setup.

From here, the more important question is whether you can sit through the quarters leading up to the clinical result.

That is why it may feel less frustrating to decide your position size and holding period first, before getting pulled in by the excitement.

Q. Even after this financing, can it still fall hard later?

The structure goes up to $30 million, so near-term pressure has eased, but the real issue is still the ELPIS II Phase 2b result in 2026 Q3. If the data is mixed or falls short of what the market wants, the second $15 million tranche may never open, and then the market could go right back to talking about discounted issuance and dilution.

Q. They call this a nano-cap biotech — so is this basically a casino trade? It feels scary.

When a stock with a market cap in the low tens of millions can jump more than 70% on one headline, it almost feels like a derivative product.

That is exactly why names like this usually make the most sense only as a very small part of a broader portfolio, using money you can afford to see swing hard.

If you draw that line clearly from the start, it gets a little easier to wait for the clinical result without feeling rushed.