CSCO -12% Plunge: Earnings Beat But Why Dumped? 75 Warning

Earnings were 'good' but stock plunged. CSCO's Q2 revenue $15.3B (+10% YoY), Non-GAAP EPS $1.04, yet margin (cost) burden and guidance interpretation overlapped, causing -12% daily drop with 3x volume surge.

💡 3-Second Investment Key Summary

- Why Moving: Q2 earnings beat but 'margin pressure + guidance disappointment' interpretation led to -12% daily plunge.

- Whale Signal: Volume at 68.01M shares, about 3x normal (22.19M)—panic deleveraging/institutional rebalancing zone.

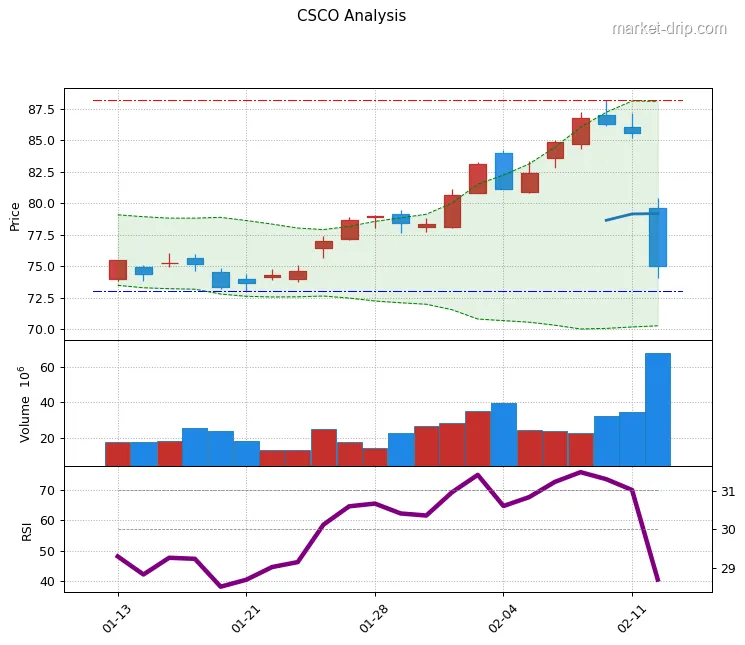

- Verdict: Hold (conservative) — below 75 is volatility zone so 'no chasing buys', confirm stability in 2-3 days first.

Market Overview

In short, today's key trigger was not the earnings itself but 'quality (margin) and next quarter confidence'.

Price Trends & Momentum

Technically, around $75 is short-term psychological line, and closing below it risks supply vacuum triggering stop/hedge orders in chain.

Key Catalysts & Risk Factors

Risks dominating price are 'margin pressure'—if cost rises persist, valuation derating accelerates even if EPS holds.

Also, guidance explicitly includes tariff impacts, so policy/cost variables growing means market likely to discount conservatively.

Recent News & Developments

squeezing margins.

Institutional & Insider Activity

Post-earnings -12% plunge typically mixes position unwinds (stops/margin call), so 'confirmed data' like insider buys/13F needs recheck at next filings.

Investment Outlook (3–12 Months)

📈 Bull Case

If AI infra orders (hyperscaler $2.1B) and networking growth (+21%) continue, and FY2026 revenue $61.2-61.7B guidance hits near upper end, 'post-plunge value re-rating' possible.

📉 Bear Case

If memory/parts cost burden lasts longer than expected, margins bend again, risking further downside (trend reversal) even on decent earnings due to 'quality issues'.

💡 Investment Strategy

Strategy is 'enter after price confirmation'. 1) On 75 recovery·hold (2-3 days) + volume normalization, approach in tranches. 2) Below 75 with volatility spike, prioritize cash weight·hedge (short-dated put/call spread) over new buys for risk management.

Frequently Asked Questions

Q. CSCO earnings were good, so why did the stock plunge so much?

Q. Can I buy CSCO right now?

Chasing buys risky until 75 reclaimed and volume calms (panic volume digested).