AMD +7.8% Surge: 3 Fatal Reasons Not to Buy Right Now

AMD surged 8%, but CEO is selling. AI chip war: NVIDIA's 85% share vs AMD 7%. Real reasons why chasing now is dangerous

💡 ⚡ 3-Second Investment Thesis

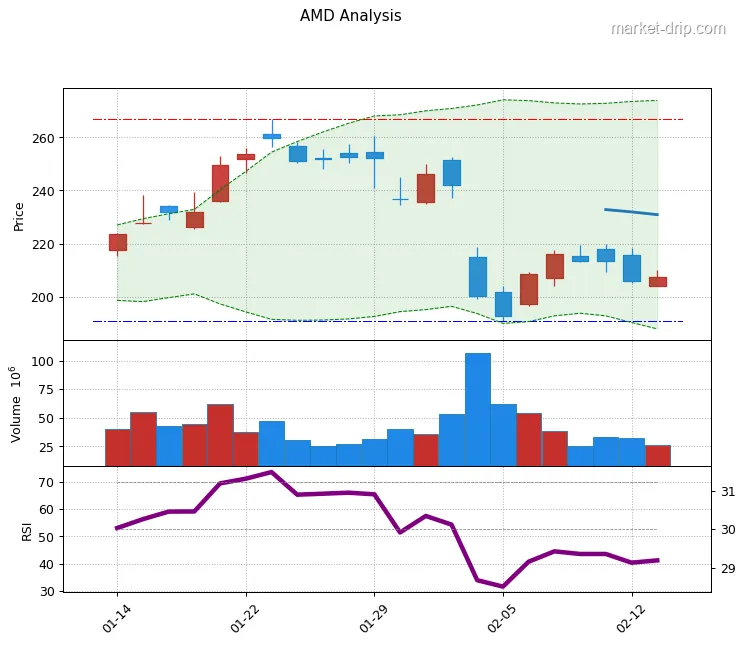

- 🔥 Surge Background: AMD surged +7.8% to $256 on Feb 15. Amazon·Alphabet's AI infrastructure spending expansion announcement and KeyBanc's '2026 server CPU sold out' forecast acted as catalysts.

- ⚠️ Hidden Risk: The wound from the -17% crash after Feb 3 earnings hasn't healed yet.

CEO Lisa Su sold ~125K shares (insider trading), AI GPU market share still severely lags NVIDIA at 7% vs 85%. - 🎯 Investment Verdict: Short-term Hold / Long-term Dollar-Cost Average Buy.

Current price $256 is 9% undervalued vs analyst avg target $282. But Q1 guidance miss risk + supply chain bottleneck (TSMC allocation shortage) gives 30% chance of re-entry to $220~$240 range.

Market Overview

But AMD's surge isn't just sympathy rally. KeyBanc analyst John Vinh raised target to $270 on Jan 13 saying "AMD server CPUs nearly sold out for 2026," and this message recirculated after 2 weeks, triggering FOMO.

Vinh forecasts AMD's MI355/MI455 AI GPUs to ship 200K units in H1 2026 alone, with AI revenue reaching $14B~$15B (3x 2024).

However, this surge is just a rebound from Feb 3 earnings shock.

AMD reported Q4 revenue $10.27B (beat estimates) but Q1 2026 guidance of $9.8B(±$300M) fell short of optimistic expectations ($10B+), causing -17% crash.

Current $256 is still -16.9% from Jan peak $308.

Key Catalysts & Risk Factors

- Current: $256.13 (Feb 15, 2026)

- Immediate Resistance: $270 (KeyBanc target & psychological)

- Key Resistance: $282~$285 (51 analysts avg target)

- Strong Resistance: $310 (high target & Jan peak)

- Key Support: $240 (50-day MA & Feb low)

- Breakdown Support: $220 (200-day MA & psychological)

Technical Indicators:

- RSI: ~65~70 estimated (entering overbought, short-term correction pressure)

- Volume: 92.88M shares (Feb 15, +111% vs 3-mo avg 43.9M) → institutional accumulation vs retail chase mixed

- Bollinger Bands: testing upper band breakout, but volatility expansion post-Feb 3 crash

Scenario Analysis:

1. Bull Scenario (40%): Break $270 → $282~$290. Conditions: ① AI GPU 200K shipment confirmation, ② TSMC allocation increase news.

2. Neutral Scenario (30%): $240~$270 range 2-4 weeks.

Wait for Q1 earnings (late April).

3. Bear Scenario (30%): Break $240 → $220 retest.

Triggers: ① NVIDIA earnings blowout highlights AMD weakness, ② China MI308 export ban ($100M) materializes.

Trader Strategy:

- Short-term (1-2 weeks): Take 50% profit near $270. RSI overheated.

- Medium-term (1-3 months): Scale in at $240. Wait Q1 earnings.

- Long-term (6+ months): Buy below $220 for 5-year hold target ($500~$600 possible, +22% annualized).

Recent News & Developments

- Revenue: $10.27B (YoY +34.1%, beat $9.67B est)

- Adj EPS: $1.53 (beat $1.32 est by +15.9%)

- Datacenter: YoY +39% growth (accelerating from Q3 +22%)

- AI GPU Revenue: ~$7B for 2025 (21% of total), 2026 target $14B~$15B

⚠️ Guidance Controversy (Q1 2026):

- Revenue Guidance: $9.8B ± $300M (midpoint YoY +32%, but QoQ -5%)

- China Risk: Includes ~$100M MI308 China exports (US regulation uncertainty)

- Non-GAAP Gross Margin: ~55% (YoY +1%p, solid but trails NVIDIA 70%+)

📈 Analyst Actions:

1. KeyBanc (John Vinh): $270 target, 'Overweight'.

Cites "2026 server CPU sold out + 10-15% pricing power".

2. Bank of America: $260→$280 upgrade. "Server CPU +50% growth in 2026, value as AI GPU alternative".

3. DA Davidson: Upgraded to 'Neutral' (Feb 14, 2026).

Not 'Buy'.

4. HSBC: Jul 2025 'Hold'→'Buy', $100→$200 target (at the time).

🚨 Insider Trading Warning:

- CEO Lisa Su: Sold ~125K shares in Feb 2026 (~$32M at market)

- EVP Forrest Norrod: Sold ~19.5K shares

- Interpretation: Executive selling = ① routine compensation exercise cash-out OR ② limited short-term upside signal.

Red flag for investors.

🔥 AI Chip Wars: NVIDIA vs AMD:

- Market Share (AI GPU, Jan 2026):

- NVIDIA: 85% (90-95% datacenter AI training GPUs)

- AMD: 7% (MI300/MI355 gaining traction)

- Others (Qualcomm etc): 8%

- AMD Strategy: ① 20-30% cheaper than NVIDIA, ② memory advantage (MI355: 288GB HBM3E vs NVIDIA B200), ③ open-source ecosystem (ROCm vs CUDA).

- Bottleneck: AMD trails NVIDIA/Apple for TSMC allocation.

X analysis estimates 2026 MI355 shipments at 250K-500K vs demand 1M+.

📅 Key Dates:

- Q1 2026 Earnings: Late April-early May 2026 (watch: AI GPU $3.5B achievement)

- MI455 Launch: H2 2026 (NVIDIA Rubin competitor)

Investment Outlook (3–12 Months)

📈 Bull Case

📈 Bull Case ($350+, 12 months):

1. AI Super Cycle Beneficiary: Amazon·Microsoft·Google plan $300B+ AI infra in 2026. AMD wins as NVIDIA alternative via Oracle Neocloud, Dell, IBM partnerships - 200K MI355 shipments = $4B revenue boost.

2. Server CPU Dominance: Fills Intel collapse void with EPYC - 2026 server CPU share 30%→40%.

KeyBanc 'sold out' diagnosis = 10-15% pricing power → gross margin 55%→57%.

3. Valuation Appeal: PEG 0.65 vs NVIDIA(1.2), Broadcom(0.9) undervalued. 2026 EPS $6.49 est = P/E 39x vs 5-yr avg(45x).

Premium to Nasdaq avg P/E 26x justified (AI growth).

4. Technical Edge: MI355's 35x perf gain (vs MI300) game-changer. 288GB HBM3E ideal for LLM inference. 10% better power efficiency vs NVIDIA B200.

5. Policy Tailwind: US CHIPS Act domestic fab support.

AMD domestic expansion = subsidy potential.

📉 Bear Case

📉 Bear Case ($180, 6 months):

1. Unbridgeable NVIDIA Gap: AI GPU share 7% vs 85% = 'uncrossable moat'.

CUDA ecosystem 10+ years vs AMD ROCm developer weakness.

Hyperscalers buy proven NVIDIA at scale.

2. Supply Chain Choke: TSMC prioritizes Apple(iPhone), NVIDIA(H200/B200).

AMD MI355 target 1M units but only 250K-500K producible → $15B revenue target risks $7B shortfall.

3. Guidance Miss Fear: Q1 $9.8B = QoQ -5% decline.

Strip $100M China = $9.7B weaker.

Conservative Q2 guidance in April = $200 collapse possible.

4. Insider Selling Signal: CEO 125K sell = 'short-term ceiling'.

Historically AMD exec selling = -8% avg 3-month return.

5. Competition Intensifies: Qualcomm, Intel Gaudi3, Google TPU, Amazon Graviton self-developed chips.

AMD risks 2nd place → 3rd-4th.

6. Valuation Trap: P/E 39x looks cheap but if 2026 EPS growth <est(+44%) at +20-30%, fair P/E 25-30x = $162~$195 target.

7. Geopolitical Risk: US-China escalation = full MI308 China export ban → $400M~$600M revenue evaporation.

💡 Investment Strategy

🎯 Final Strategy (Risk-Adjusted):

Current ($256) Verdict: Short-term Hold + Long-term DCA Buy

Position Strategy:

1. Already Holding (avg cost <$200):

- ✅ Hold.

Target $350 (mid-2027) take 50% profit.

- ⚠️ Stop loss: $220 break sells 30% (wait re-entry).

2. New Entry:

- ⛔ No full position now.

RSI overheated + +7.8% spike = correction risk.

- ✅ 3-Step Scale In:

- Stage 1 (30%): $240~$245 (50-day MA support)

- Stage 2 (40%): $220~$230 (200-day MA, Q1 miss scenario)

- Stage 3 (30%): <$200 (panic selling, 15% odds)

3. Short-term Trading (1-4 weeks):

- 🎲 High risk/reward: Buy $256 → $270 target (+5.5%).

Stop $248 (-3.1%).

- Conditions: Daily vol >80M shares + RSI <75.

4. Long-term (3-5 years):

- ✅ Core position: <$220 entry. +22% annualized = $600 by 2030 (+134%).

- 📌 No dividend → growth focus required.

Portfolio Allocation:

- No solo AMD.

Mix 50% semi ETF(SMH,SOXX) or AMD 30% + NVDA 40% + TSM 30%.

Risk Management Checklist:

- [ ] Q1 earnings (late April) calendar alert

- [ ] Monitor NVDA earnings (Feb 26 expected) → AMD relative valuation

- [ ] Track TSMC monthly revenue (10th each month) → AMD allocation estimate

- [ ] Weekly insider trading site check (more selling = warning)

Key Message: AMD = 'AI #2 stock charm AND trap'.

Clear undervaluation vs NVIDIA but real tech/ecosystem gap too. <$220 entry = multi-bagger potential, but >$270 chase = 30% short-term loss risk.

Emotion-free mechanical DCA is answer.

Frequently Asked Questions

Q. ❓ Why did AMD surge +7.8% on Feb 15?

NVIDIA also +7.8%.

But AMD-specific catalysts: ① KeyBanc's '2026 server CPU sold out' forecast recirculated after 2 weeks triggering supply shortage FOMO, ② oversold rebound demand post-Feb 3 -17% earnings crash.

Volume 2x+ normal (92.88M shares) = institutional accumulation + retail chasing.

Q. ❓ Is AMD a buy right now?

Analyst avg $282 = +10% upside but risk/reward unattractive. Recommended: ① New entry wait <$240 (50-day MA), ② Holding = partial profit $270 then re-buy $220, ③ Long-term DCA <$220 but cap portfolio at 30%.

AMD trails NVIDIA tech/ecosystem(7% vs 85% share) so diversification essential.

Q. ❓ AMD vs NVIDIA - better investment?

AMD faces Q1 guidance miss + supply(TSMC allocation) risks.

Long-term(3-5yr): AMD better risk/reward.

Reasons: ① PEG 0.65 vs NVDA 1.2 undervalued, ② NVDA $1.3T limits growth, AMD $397B has 2x room, ③ AI chip diversification(Qualcomm, Intel entry) favors AMD as #1 beneficiary.

Conclusion: Conservative = NVDA, Aggressive = AMD 30% + NVDA 40% + Cash 30% portfolio.

Q. ❓ Is CEO Lisa Su's 125K share sale bad news?

Exec selling = ① routine stock option exercise cash-out (normal) OR ② limited short-term upside judgment (warning).

Lisa Su timing problematic - selling post-Feb 3 -17% crash rebound ($250-260 est) = 'top recognition' signal.

Historically AMD exec selling = -8% avg 3-month return, so expect short-term pullback($240 target).

Q. ❓ Can AMD's AI chips(MI355/MI455) catch NVIDIA?

MI355 = 35x perf vs MI300, 288GB HBM3E ideal for LLM inference matching/exceeding NVIDIA B200 in spots. 20-30% cheaper attracts Oracle, MSFT as 'backup supplier'.

But 3 barriers:

1. Software: NVIDIA CUDA 10+yr developer base(99%) vs AMD ROCm compatibility/tool gaps.

2. Supply: TSMC allocation trails Apple/NVIDIA - 2026 1M target but 250K-500K producible.

3. Inertia: Hyperscalers(AWS,Azure,GCP) invested billions in proven NVIDIA. Switch costs massive.

Conclusion: AMD 7%→15% share growth possible(2027 target) but NVIDIA overtake = 2030+.

Invest as 'market expansion beneficiary' not 'NVIDIA replacement'.

Q. ❓ What's AMD's 2026 price target?

- Average: $282.82 (+10.4% from current)

- High: $310 (bullish, Jefferies/KeyBanc)

- Low: $140 (bearish conservatives)

Scenario Targets:

1. Bull ($350, 25%): MI355 500K shipments + AI revenue >$15B + server CPU 40% share.

2. Base ($280, 45%): Q1-Q2 guidance met + relative valuation vs NVDA improves.

3. Bear ($200, 30%): Supply bottlenecks + Q1 miss + NVDA dominance marginalizes AMD.

Long-term (2030): Some analysts target $500-600 (+22% annualized).

Requires AI market 30% CAGR + AMD 20% share.